AI Spread Faster Than the Internet – But 62% of Users Got Stuck at the Start

In April 2026, Stanford HAI released its ninth annual AI Index Report – the most comprehensive overview of the state of the AI industry. The headlines are predictably optimistic: corporate adoption reached 88%, generative AI outpaced the internet in diffusion speed, and the consumer value of GenAI tools is estimated at $172 billion annually. But look behind the numbers – and a familiar problem emerges.

At mysummit.school, we analyzed the Epoch AI / Ipsos data in a separate piece: 62% of users apply AI superficially – for one or two quick tasks. Now Stanford AI Index 2026 provides context for that figure. Adoption has happened. Tools are available. Investment is breaking records. And yet most people haven’t moved beyond their first encounter.

This is the first article in the “Stanford AI Index 2026” series. It covers the paradox of mass adoption: how a technology that spreads faster than any predecessor manages to leave behind those who are formally already using it.

What the report covers

The Stanford AI Index is an annual fact-based report that aggregates data from dozens of sources: from McKinsey and Epoch AI to government databases and academic publications. The ninth edition was published in April 2026 and covers data for 2025.

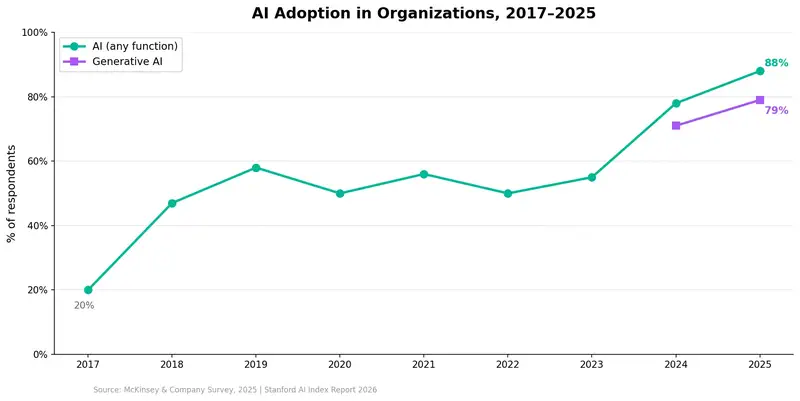

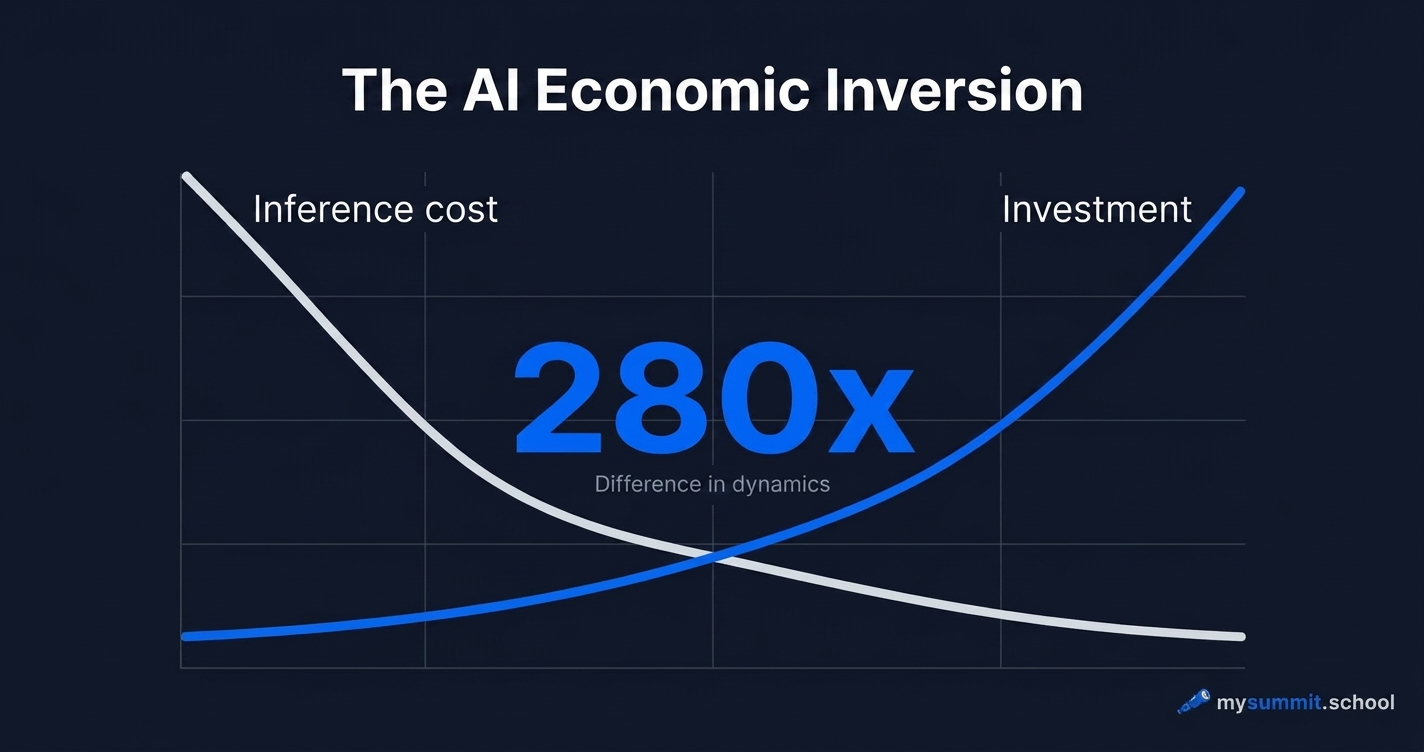

What distinguishes the ninth edition from the eighth. Last year’s AI Index 2025 (eighth edition, 2024 data) captured a turning point: corporate adoption jumped from 55% to 78% in a year, compute costs became the key barrier, and inference costs dropped 280x since 2023. Back then, the main storyline was the leap in model capabilities – SWE-bench went from 4.4% to 71.7%.

In 2026, the focus shifted. Technical benchmarks are still climbing, but the main story is adaptation – who actually adopted AI, how fast it’s happening, and what value it creates (or doesn’t). For the first time, the report devotes a separate chapter to consumer value of GenAI, and the topic of “AI and employment” received significantly more data than before.

Speed no technology has ever matched

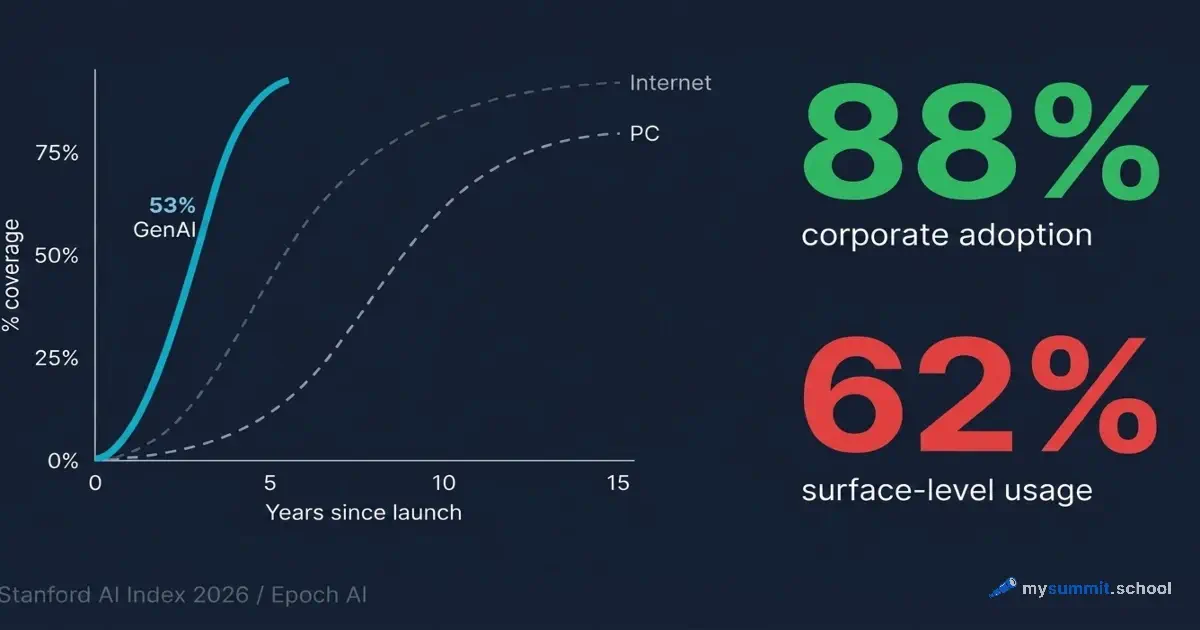

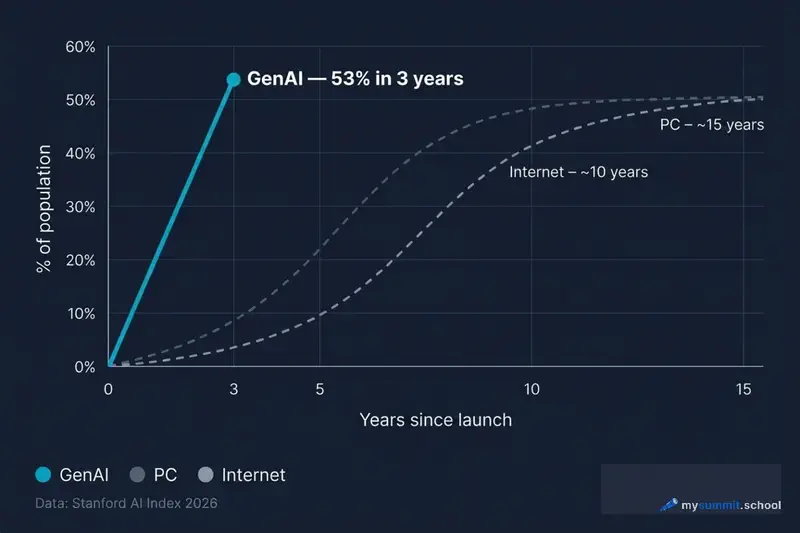

Let’s start with what truly impresses. Generative AI reached 53% population coverage in three years. The personal computer took nearly 15 years, the internet – about ten. No consumer technology has ever spread this fast.*

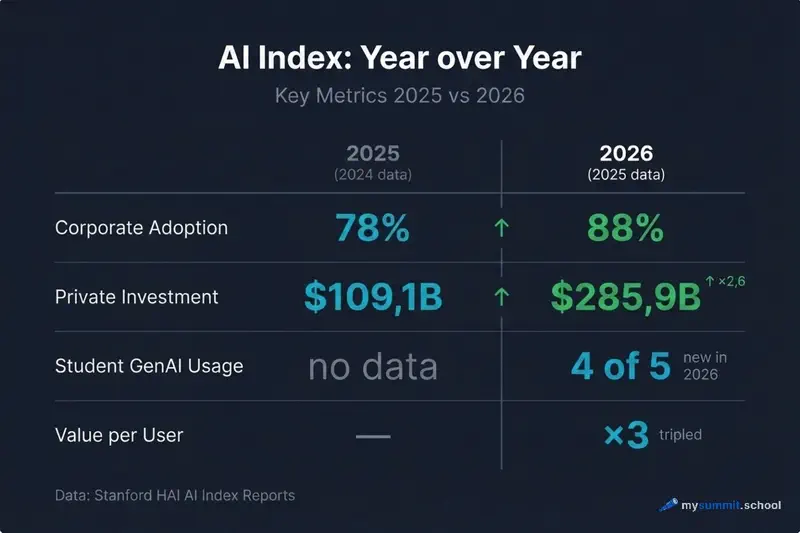

And this isn’t about abstract “awareness of existence.” The consumer value of GenAI tools, according to the AI Index, is $172 billion per year for American consumers. Median value per user tripled between 2025 and 2026. Four out of five university students use generative AI in their studies.

But here’s where it gets interesting. Adoption speed is uneven – and the gap between countries turns out to be larger than expected. Singapore leads with 61% regular GenAI usage, the UAE at 54%. And the United States, despite being where the vast majority of tools and investments originate, ranks just 24th at 28.3%.

Think about it: the country that produces ChatGPT, Gemini, Claude, and Copilot trails Singapore in adoption by more than two to one. This is not a story of “technology leadership = user leadership.” Creating technology and adopting technology turn out to be entirely different skills.

* The comparison is approximate – PC and internet data use different methodologies, and the AI Index acknowledges this. But the order-of-magnitude difference is telling.

Year over year: AI Index 2025 vs 2026

The numbers become even more striking when you place the two reports side by side.

Corporate adoption grew from 78% to 88%. A year earlier, this metric jumped from 55% to 78% – and that already seemed rapid. Ten percentage points in a year on an already high base means AI has stopped being an “experiment for early adopters” and became an operational norm. 88% of organizations report using AI in some form.

Note the phrasing – “in some form.” We’ll come back to that.

Private investment grew from $109.1B to $285.9B – a 2.6x increase in a year. In 2024 (AI Index 2025), GenAI investments alone totaled $33.9B. The total private AI investment for 2025 – $285.9B – exceeds the GDP of many countries. The main driver is infrastructure: data centers, compute, chips. Money is flowing into the foundation, not into applications.

The number of AI incidents continues to rise. In 2024, the AI Index recorded 233 cases (deepfakes, data breaches, automation errors). The 2025 trend goes in the same direction – more usage means more incidents. This isn’t a catastrophe, but it’s the cost of scaling that rarely gets factored into ROI models.

For those who built business cases on last year’s data – we analyzed the ROI justification methodology using concrete Google Cloud figures. AI Index 2026 data strengthens the argument: the market is doubling, not stabilizing.

Numbers alone are context. What to do with them in practice is a separate skill.

9 free lessons on using AI for real manager tasks. Report data is context. Skill is what you can actually try.

No payment required • Get notified on launch

The depth paradox: 88% adopted, 62% stuck

And here we arrive at the central contradiction. 88% of organizations use AI. Generative AI outpaced the internet in adoption speed. Investments tripled. Students have built ChatGPT into their studies. Everything points to mass adoption.

But.

Epoch AI / Ipsos data, which we analyzed in detail in April, paints a different picture: 62% of AI users apply it at the level of “one or two quick tasks.” Only 5.6% rely on AI seriously – regularly, deeply, for core work processes.

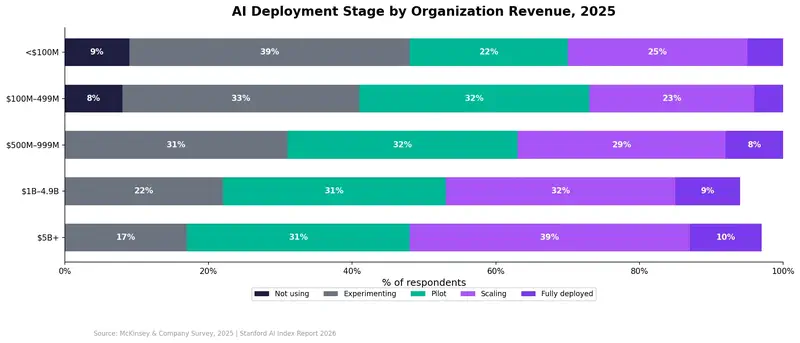

This isn’t a contradiction between two reports. It’s the same reality seen from different angles. The Stanford AI Index counts “adoption” – an organization uses AI in at least some way. Epoch AI counts “depth” – how a specific person actually works with that AI. And the gap between “somehow” and “seriously” turns out to be enormous. Even among companies with revenue above $5B, only 10% have “fully deployed” AI. For smaller companies – 3–5%.

I’d call this the accessibility paradox: the easier it is to try a technology, the more people get stuck at the “tried it” stage. The entry barrier vanished – but that didn’t help with the deepening barrier. Anyone can open ChatGPT and ask a question. Restructuring a work process around it is an entirely different task.

The Stanford AI Index indirectly confirms this gap. Consumer value data shows that median value per user tripled – but this is a median that includes heavy users who create disproportionately more value. If 5.6% use AI ten times more intensively than the rest, they move the median even if the remaining 62% stand still.

Productivity rises – while junior positions disappear

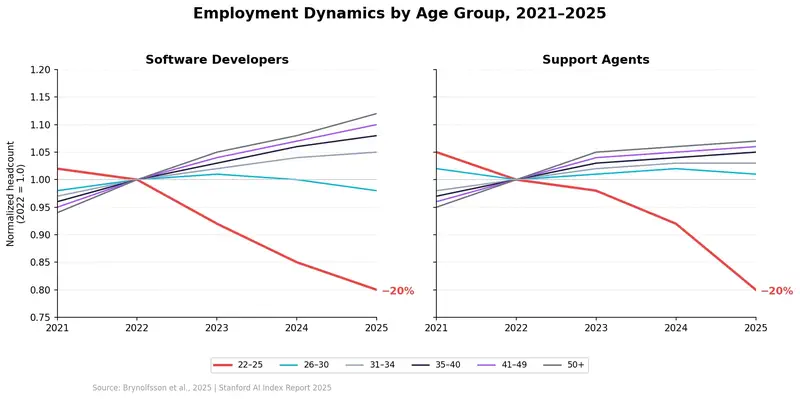

Another AI Index 2026 storyline worth examining separately. The report records consistent productivity gains: 14% to 26% depending on the sector. Customer support and software development are the two areas where the effect has been measured most reliably.

This is good news – but it has a flip side.

In those same areas – customer support and development – junior positions are starting to decline. The report provides a specific figure: employment among American developers aged 22–25 has dropped nearly 20% since 2022. This isn’t a recession. It’s a structural shift.

The mechanism is clear: AI takes over tasks that entry-level specialists used to handle. Document drafts, first-line support, boilerplate code, basic analytics. These are precisely the tasks where juniors learned and proved their value. When AI does them faster and cheaper, demand for entry-level workers drops – even as demand for experienced specialists grows.

For managers, this creates a non-obvious dilemma. Team productivity may rise thanks to AI, but the pipeline for developing new talent narrows at the same time. Who will become an experienced specialist in three to five years if today there are fewer tasks for beginners to grow on?

This isn’t an abstract argument. We analyzed the real cost of AI tools for dev teams – and the same logic applies: a tool that saves a senior’s time simultaneously shrinks the growth space for a junior. Efficiency and development end up in conflict.

The depth paradox and the impact on employment are two sides of the same problem: the tool is accessible, but the skill to use it – is not.

A manager doesn't need to become a developer. You need to understand which tasks AI does better and where it creates new problems. Open module – free.

No payment required • Get notified on launch

What this means for a manager

Of all the AI Index 2026 figures, I’d highlight three conclusions with direct relevance to management decisions.

“We adopted AI” is no longer an argument. When 88% of organizations already use AI, adoption alone doesn’t create competitive advantage. The advantage lies in depth – in whether an organization has moved from “we have ChatGPT” to “AI is embedded in three key processes and we’re measuring results.” Most haven’t made that move. That’s an opportunity for those who will.

Adoption speed is deceptive. 53% coverage in three years is phenomenal as a slide number and nearly meaningless as a real-impact metric. Because “using” and “getting value” are different things. Four out of five students use GenAI, but that doesn’t mean four out of five became more productive. An adoption metric without a depth metric is half the picture.

The window for cheap experiments is closing, but the depth window is open. Investment grew from $109B to $286B in a year. Infrastructure is getting more expensive. Competition for talent is intensifying. The cost of mistakes is rising – not because tools got worse, but because stakes got higher. Yet the gap between “using superficially” and “using systematically” is still determined not by budget, but by skills. The 62% didn’t get stuck because they couldn’t afford a subscription.

What’s next in the series

This is the first of five articles on Stanford AI Index 2026. In the rest:

- The economics of models: how a 280x drop in inference cost changes ROI calculations

- The jagged frontier of capabilities: olympiad math – yes, analog clocks – no

- The perception gap: 73% of experts believe in AI, 23% of the general public

- The education gap: why 80% of students use AI, but formal education lags behind

Each of these themes affects how a manager should make AI adoption decisions – not “in general,” but specifically: what to buy, whom to hire, what to expect.

From numbers to skills

Stanford AI Index shows: AI adoption is no longer the question. The question is depth. The MySummit.school course starts exactly where 62% got stuck: moving from one-off queries to systematic AI use in management tasks.

Stanislav Belyaev

Engineering Leader at Microsoft18 years leading engineering teams. Founder of mysummit.school. 700+ graduates at Yandex Practicum and Stratoplan.