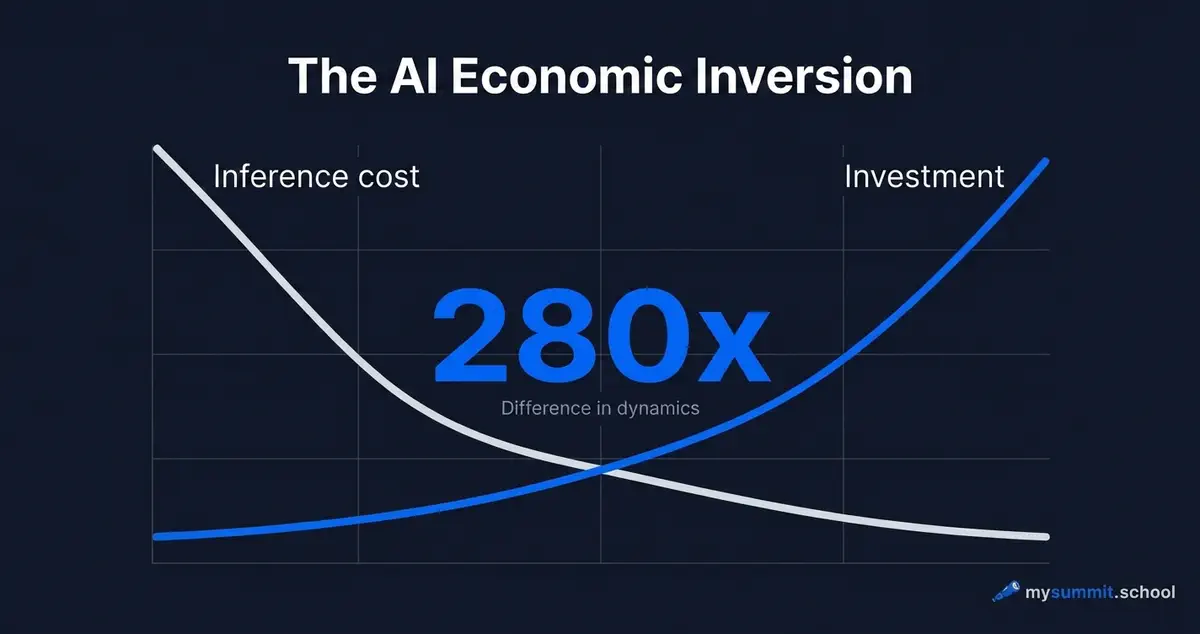

280x Cheaper in Two Years: The AI Economy Has Flipped

In 2023, a single query to GPT-4 cost enough that you had to count carefully. In 2025, the equivalent query became 280 times cheaper. Not 280 percent – 280 times. In two years, the cost of using AI went from a barrier to a rounding error.

Stanford AI Index – the annual report that compiles data on the AI industry from hundreds of sources – flagged this collapse in its 2025 edition. The 2026 report added context: AI investment exploded to $285.9bn, consumers are extracting $172bn of value a year, and data centres are eating electricity at the scale of New York State. The economy flipped – just not the way most people expected.

280x – what happened to cost

Stanford AI Index 2025 introduced a metric that deserves its own paragraph: the cost of inference on GPT-3.5-class models dropped 280 times since ChatGPT launched in late 2022. This isn’t the effect of swapping an expensive model for a cheap one. It’s a price collapse at comparable quality – driven by competition between providers, infrastructure optimisation, and cheaper chips.

For context: over the same period smartphones got cheaper by something like 15 percent. Cloud storage by maybe 30 percent. Airfares – basically not at all. AI inference – 280 times.

We see this in our own data. When we tested 53 models in spring 2026, the cheapest query cost $0.0001 and the most expensive $0.17. A 1,600x spread in price. The spread in quality between the top ten was 0.24 points out of five. A market where price falls faster than quality rises is a market that has flipped.

Practically, this means one thing: access to AI is no longer the problem. In 2023 a manager could plausibly say “we don’t have the budget for GPT-4.” In 2026, that sounds about like “we don’t have the budget for email.” Budget models like Qwen3.5 9B or DeepSeek V3.2 deliver 85–90% of flagship quality for fractions of a cent per query. For drafting an email, summarising a document, or prepping a meeting agenda – you won’t notice the difference between a $0.0002 model and a $0.016 one.

The barrier has shifted. It’s no longer the price of access, it’s the skill of using it.

The money is flowing

While the cost of use was collapsing, the volume of investment did the opposite.

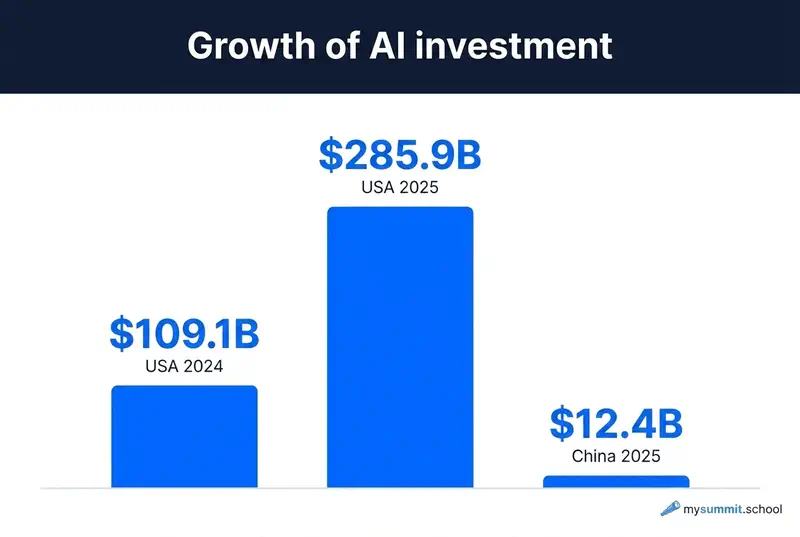

AI Index 2026 records private AI investment in the US hitting $285.9bn in 2025. A year earlier it was $109.1bn. A 2.6x jump in a single year. In absolute terms, more than the GDP of most countries on the planet.

Second place – China at $12.4bn. That’s 23 times less than the US. Stanford does add a caveat: the Chinese figures don’t capture state funds and investment through state-owned companies, which play a different role in China than venture capital does in the American ecosystem. The real gap is probably smaller. But even with that adjustment, the scale of American dominance is striking.

Another number: 1,953 new VC-backed AI companies appeared in the US in 2025. That’s ten times the nearest country. Not two times, not three – ten.

Where does the money go? Global compute for AI has been growing 3.3x annually since 2022 and has reached 17.1 million H100-equivalents. Nvidia controls more than 60% of that capacity. The cost of training frontier models keeps climbing – even as inference gets cheaper. Training a model and using one are two different economies, moving in opposite directions.

Here’s a thought experiment: if inference is 280 times cheaper and investment is 2.6 times higher, then usage volume has grown by orders of magnitude. The money didn’t disappear – it migrated from per-query payments into infrastructure spend. The user pays less. The system as a whole pays more.

Consumer value – $172bn

AI Index 2026 cites an estimate worth pausing on: the consumer value of generative AI for Americans is $172bn a year. That isn’t company revenue and it isn’t market size – it’s an estimate of the benefit people get, many of whom pay nothing.

Median value per user tripled between 2025 and 2026. That’s an unusual dynamic. Normally, as a technology spreads, per-user value falls – new users are less engaged than the early ones. Here it’s the opposite. Either users are learning fast how to extract more value, or the tools got meaningfully better, or some combination of the two.

But here’s the awkward bit: $172bn of value against $285.9bn of investment is not yet the kind of balance that should make investors comfortable. Of course, consumer value and revenue are different things. Of course, investment is a bet on the future, not a purchase of today’s output. Still, the question stands: who, and when, starts converting that benefit into money?

The numbers explain why value is being created in principle. How it shows up on a manager’s actual tasks is a conversation that starts not with a report but with practice.

How to turn AI from a fun toy into a tool with measurable results? 9 manager tasks with AI – free.

No payment required • Get notified on launch

An expensive model is not a better model

The collapse in inference cost creates a paradox we worked through in detail in our 53-model analysis: if a cheap model gives you 99% of the quality of an expensive one, what exactly are you paying for when you pick the premium option?

The key numbers, briefly: the price gap between the cheapest and the most expensive model in our benchmark was 1,600x. The quality gap across the top ten was 0.24 points. Models in the $0.001–0.003-per-query range consistently scored 4.4–4.7 out of five on management tasks. The flagships – 4.7–4.8.

Stanford AI Index confirms this at the macro level: the inference cost crash wasn’t accompanied by a proportional drop in quality. Models got cheaper and better at the same time. This isn’t a zero-sum trade.

For a manager, that means the “premium vs budget” framing is a false dilemma. The right question is “which model for which task.” The bulk of AI spend usually hides not in the per-token API price but in integration, training people, and time lost to inefficient use.

Of course, for the top 20% of tasks – strategic analysis, ambiguous data, materials going to leadership – the gap between models is real and justifies the markup. But for the other 80%, paying for premium is exactly what we’ve called the “AI tax”: spending that feels like investment and behaves like habit.

The hidden costs

So far we’ve talked about how AI got cheaper for the user. Now: what that cheapness costs the system.

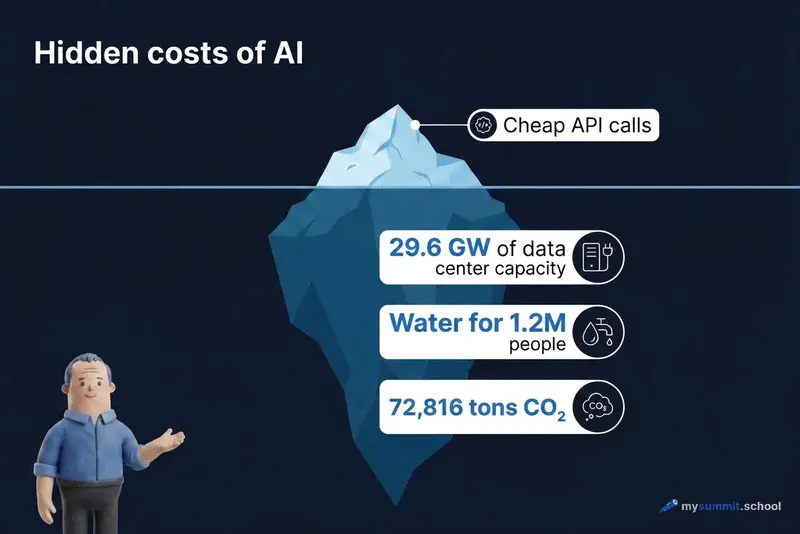

AI Index 2026 reports numbers that rarely make it into provider marketing materials.

AI data centre capacity has reached 29.6 gigawatts. For comparison – that’s comparable to the peak electricity load of New York State. Not Manhattan – the whole state. And that’s current capacity, before counting announced builds.

CO₂ emissions from training frontier models climb with each generation. Stanford estimates that training Grok 4 cost roughly 72,816 tonnes of carbon dioxide. For scale: the annual footprint of a small city.

But possibly the most unexpected figure is water. GPT-4o inference may consume more water than is needed to supply drinking water for 1.2 million people. Not training – inference. Every query, every email draft, every “summarise this document.” Multiply by hundreds of millions of users.

This is one of those cases where “free for the user” doesn’t mean “free.” The cost has shifted from a manager’s budget to the planet’s energy budget. I’m not sure the industry has a coherent answer to this – so far the conversation mostly reduces to plans for nuclear and renewables that exist mainly in press-release form.

Environmental footprint, legal risks, choosing the right tool for the job – try AI on 9 real manager tasks. Free.

No payment required • Get notified on launch

What this means for a manager

So: in two years the cost of using AI fell 280-fold, while annual investment grew to $286bn. In parallel, consumer value for Americans alone reached $172bn – and the bill is being paid in electricity and water at a scale that would have seemed absurd for an information service not long ago.

What of this actually matters in practice?

First: access to AI is a solved problem. If you or your team aren’t using AI at work, it isn’t the price. It’s something else – not knowing where to apply it, no skill at formulating tasks, fear of getting the wrong answer, corporate policies that haven’t caught up. All of those are real barriers. None of them are about money.

Second: the gap between models is shrinking, and the gap between users is widening. Google Cloud’s ROI report shows that companies actually getting returns from AI don’t get them by buying an expensive model, but by matching the tool to the task and training people. A $0.002 model in the hands of someone who knows how to frame a task gives you more than a $0.17 model in the hands of someone typing “make it look nice.”

Third: the environmental cost isn’t an abstraction. It’s a factor that will start showing up in regulation, pricing, and corporate reporting. It doesn’t change your budget today. But if you’re building an AI strategy on a two- or three-year horizon, it’s worth pricing in.

And here’s what I think tends to get lost in the “cheapness revolution” conversation. Yes, AI is available to everyone. But availability of the tool and the ability to use it are different things. There’s a hammer in every house, and that doesn’t make everyone a carpenter. The cost of AI fell 280-fold. The cost of learning to work with it didn’t.

That, possibly, is the real shift of 2025–2026. Competitive advantage moved from “we have access to AI” to “our people know how to work with it.” The first now costs fractions of a cent per query. The second – still expensive, slow, and without guarantees.

But if $172bn of consumer value is already being generated, someone is building those skills. The only question is how fast you are.

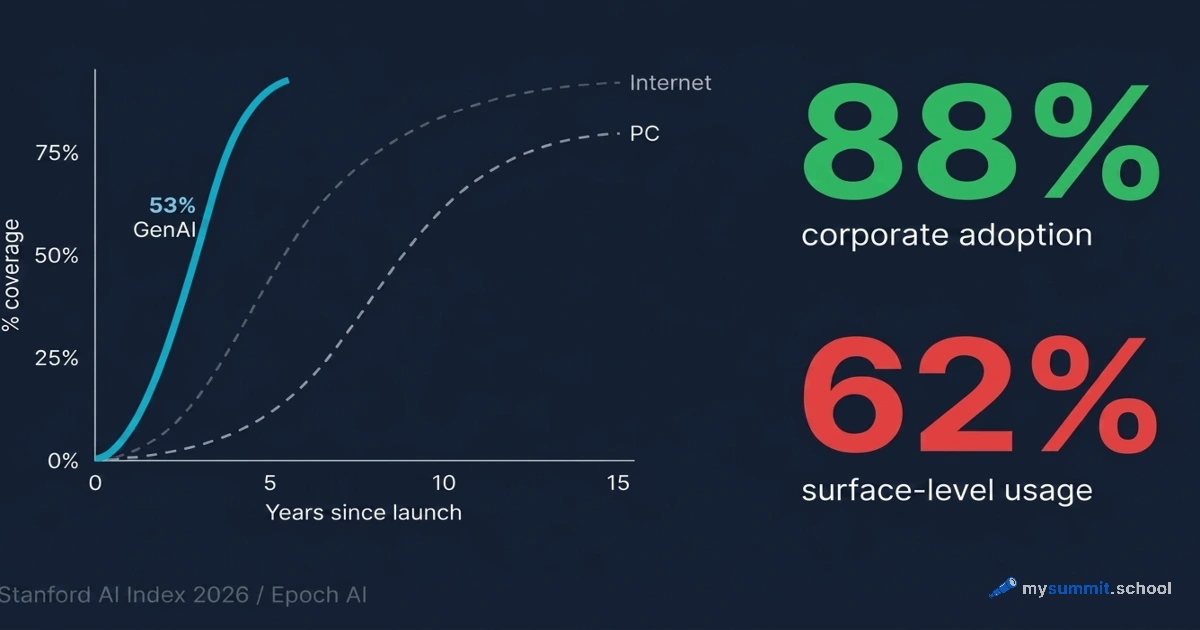

This is the second piece in the “Stanford AI Index 2026” series. The first was about the adoption paradox: why, given how much cheaper AI has become, deep usage remains rare. The next one is about the “jagged frontier” of AI capability: tasks where models already beat experts, and tasks where they still fail.

Access is solved. Skill remains.

A $0.002 model in the hands of a trained manager delivers more than GPT-5 in the hands of a novice. The MySummit.school course covers prompt engineering, critical thinking with AI, safe handling of data, and tool selection strategy.

Stanislav Belyaev

Engineering Leader at Microsoft18 years leading engineering teams. Founder of mysummit.school. 700+ graduates at Yandex Practicum and Stratoplan.